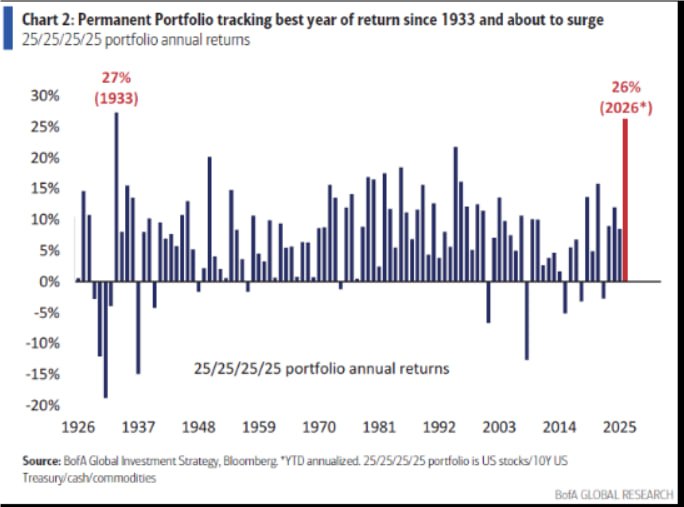

Equal 25% allocations to stocks, bonds, cash, and commodities — often referred to as an “all-weather” or risk-parity-style portfolio — is delivering its best year since 1933, up 26% year-to-date in its third-largest outperformance versus the traditional 60/40 allocation in a century, according to Bank of America strategists.

This exceptional performance reflects a rare macro environment where all four asset classes are simultaneously contributing positive returns.

The magnitude of outperformance versus 60/40 suggests a structural shift in market dynamics: higher inflation volatility, regime uncertainty, and increased correlation breakdowns are undermining the traditional stock-bond diversification assumption. In contrast, the equal-weight multi-asset approach is capitalizing on dispersion across asset classes rather than relying on a single dominant driver.

Importantly, such strong performance historically tends to occur during transition regimes — typically following major macro dislocations (e.g., 1930s, 1970s, early 2020s) — when policy, inflation, and growth trajectories are simultaneously in flux.